Fire Insurance vs Houseowner/Householder Insurance: Everything You Need To Know.

The home-buying process can be overwhelming, especially for first-time homeowners. If you’re in the midst of buying a home, there’s a good chance you’ve already heard about fire insurance and why you need it.

In fact, many Malaysians first learn about fire insurance when applying for a housing loan. Due to its extreme importance, banks require it before approving a loan; so it becomes part of the home-buying process.

But here’s a question many homeowners don’t think about until later: is fire insurance enough to protect your home from other unforeseen circumstances?

To answer that, it helps to understand how fire insurance works and how it compares with Houseowner/Householder Insurance.

When To Buy Fire Insurance?

After you’ve signed the Sale and Purchase Agreement (SPA) for your property, the bank begins processing your housing loan. Because the house acts as collateral for the loan, the bank will usually require fire insurance for the property before it releases the loan.

Once the policy is arranged, the bank is typically listed as the beneficiary since it is financing the property. After that, the loan can be disbursed, and the purchase can move forward.

What Does Fire Insurance Cover in Malaysia?

Fire insurance provides coverage for fire-related risks, this includes:

- Fire outbreak

- Lightning

- Domestic gas explosions

This type of insurance protects the structure of the property, such as the walls, roof, and built-in fixtures. This is why fire insurance is considered basic protection because it does not cover other potential risks to your home and it does not provide coverage towards your belongings.

Is Fire Insurance Enough To Protect Your Home?

No, fire insurance is not enough to protect your home. Because it’s required by the bank, it’s easy to assume that fire insurance is the main protection your home needs. But the truth is, it only covers a limited set of risks and the bare minimum

More common circumstances such as floods, windstorms, and theft are usually not included unless additional coverage is added.

And here’s what we know as homeowners: unexpected incidents at home don’t always involve fire.

Why Do You Need A Houseowner/Householder Insurance Policy?

Now that we know that fire insurance is not sufficient for your peace of mind when it comes to protecting your home, it’s time to look at Houseowner/Householder insurance as an umbrella to all your home protection needs.

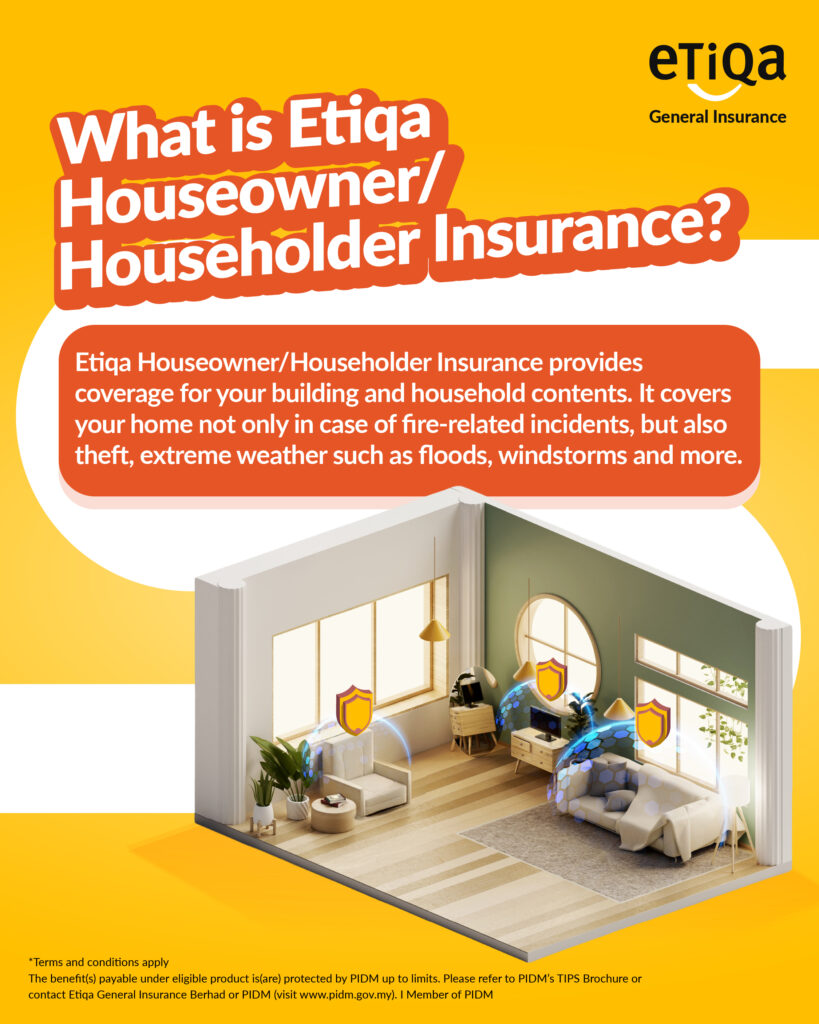

Etiqa Houseowner/Householder Insurance provides coverage for your building and household contents against fire, theft, extreme weather such as floods, windstorms and more.

Fire Insurance vs Etiqa Houseowner/Householder Insurance

Fire Insurance is typically limited to coverage against fire, lightning and domestic gas explosion while Houseowner/Householder Insurance entails other potential risks, detailed in the table below:

| Coverage | Fire Insurance | Etiqa Houseowner/Householder Insurance |

| Fire | ✓ | ✓ |

| Lightning | ✓ | ✓ |

| Domestic gas explosion | ✓ | ✓ |

| Theft by actual forcible and violent breaking into the house | – | ✓ |

| Extreme weather/Natural Disasters (flood, hurricane, cyclone, typhoon, windstorm, earthquake) | – | ✓ |

| Loss of Rent – Limit 10% of Total Sum Insured | – | ✓ |

| Liability to third parties for accidents in your house – Limit of Liability up to RM50,000 | – | ✓ |

| Contents temporarily removed from the house – Limit 15% of the total sum insured on contents | – | ✓ |

| Damage to mirrors, other than hand mirrors – Limit RM500 per piece for any one accident | – | ✓ |

| Compensation on Death of the Insured Person; due to fire or robbery where there is violent and forcible entry to the house – Limit RM10,000 or one-half of the Sum Insured on contents, whichever is lower | – | ✓ |

| Domestic helper’s property | – | ✓ |

Take Action! Sign Up For Etiqa Houseowner/Householder Insurance

1. Review your current home protection plan

If you already have home insurance, it might be a good time to review whether your home protection is comprehensive and not limited to fire-related incidents only. Many homeowners today choose broader protection that also includes risks like floods, burst pipes, theft and other unexpected events.

2. Sign up online for Etiqa Houseowner/Householder Insurance

With Etiqa Insurance Houseowner/Householder Insurance, you can protect both the structure of your home and the belongings inside it under one plan while being prepared for more than just fire-related incidents.

Did you know, you get 25% off your policy when you sign up online?

3. Customise your home protection plan with extra coverage

You can also consider expanding your coverage with optional add-ons for extra protection. This way, your home is safeguarded against unexpected situations.

Optional add-ons available with Etiqa include:

- Riot, Strike and Malicious Damage

- Increase limit for loss of rent

- Inoccupancy in excess of ninety (90) days

- Theft without actual forcible and violent breaking into and/or out excluding theft by domestic servants or members of family/household

While fire insurance may be a good start to protecting your home, a houseowner/householder insurance policy is a more suitable option, providing coverage for your home and belongings beyond fire-related risks.

The information contained in this blog is provided for informational purposes only, and should not be construed as advice on any matter. Etiqa accepts no responsibility for loss which may arise from reliance on information contained in the article. This information is correct as of 4th February 2026

The benefit(s) payable under eligible product is(are) protected by PIDM up to limits. Please refer to PIDM’s TIPS Brochure or contact Etiqa General Insurance Berhad or PIDM (visit www.pidm.gov.my). I Member of PIDM.